New Social Security Commissioner Cuts Clawbacks!

- Social Security Commissioner Steps Up! | Terry Savage - March 26, 2024

- How Social Security's overpayment mistakes can become your responsibility | 60 MINUTES

-

New Social Security Commissioner Cuts Clawbacks!

-

There's nothing more painful than losing your job when you're older and not being able to get a new one.

Research says there's a stigma about "older unemployment" - especially when it drags on for more than a year!

Meet Ben who is going through that right now. He remains optimistic, but details the hazards -- even for those in technology -- when a job disappears. Some helpful perspective for you - or someone you might know and love.

-

The price of prescription drugs can be enormous when you're on Medicare, so in this Friends Talk Money episode, we offer advice on how to pay the least for your medications. With help from expert Diane Archer of JustCareUsa, we discuss when to use your Medicare Part D plan, what to know about prescription discount cards and programs from drug companies and states that can lower your prescription costs.

-

You're probably familiar with financial literacy, which entails having the skills, knowledge and behaviors to make decisions about money. But how's your longevity literacy? Not sure what we're talking about? In this episode Pam, Terry and Richard break down longevity literacy, and explain the impact, especially when it comes to your retirement readiness. Guest expert, Surya Kolluri, who is the head of the TIAA Institute joins the Friends Talk Money crew to uncover the importance behind longevity literacy and why he believes more Americans should focus on improving theirs.

-

In this episode Pam, Terry and Richard talk about what’s likely to be the most important financial decision you’ll ever make… what to do with your 401(k) money when you’re ready to retire? The Department of Labor says any retirement advice you get a work should always be in your best interest. The question is… is it? Pam leads the discussion about the DOL’s new proposed Fiduciary Rule and includes special guest Kevin Walsh of Groom Law Group and break down why the DOL’s so worried.

-

Advice on lowering your debt load and credit card rates, plus pros and cons of filing bankruptcy. With Bruce McClary, Senior Vice President of Media Relations & Membership at the National Foundation for Credit Counseling.

-

Retiring abroad can be appealing, with lower costs and great weather. But here are some things you also need to consider before making a move.

In this episode, the Friends Talk Money team discusses how you can help set up your grandchildren for financial success beyond the traditional 529 college saving plans. Tune in as Pam, Richard and Terry share helpful tips and savvy money strategies that they’ve learned from their own personal experiences.

-

The rules for RMDs have changed and you will want to know how much you must take out of your retirement plans and when. We explain it all on this episode of Friends Talk Money, including year-end advice.

Required Minimum Distributions:

The Friends Talk Money podcasts talk about why many of us aren't bestowing inheritances to heirs the right way and not helping our parents make inheritances properly. We also talk about how financial advisers could be more helpful to families so they handle inheritances wisely.

-

Social Security is clawing back $21 billion in mistaken overpayments — impacting retirees and the disabled. Terry Savage and Larry Kotlikoff have written a new book — Social Security Horror Stories — revealing the shocking abuse. Last weekend they were featured on CBS - Sixty Minutes speaking with Anderson Cooper about this issue. In this episode, Larry joins Terry, Pam and Richard to take a deeper dive into problem and what you should do to ensure you get what’s rightfully yours.

-

What to know about Medicare Open Enrollment for 2024. What’s new and how to shop wisely for coverage.

-

Not everyone looks at their personal financial future through rose colored glasses. In fact a recent Gallup poll shows Americans not yet retired are more worried than anytime in the past ten years. Discouraged savers who see the glass-half-empty may actually need different financial strategies just based on their outlook. We give you solid financial planning tips that can make your outlook.

-

Roger AKA, "The Retirement Answer Man” and author of “Rock Retirement: A Simple Guide to Help You Take Control and Be More Optimistic About the Future,". Roger has been a CERTIFIED FINANCIAL PLANNER™ professional for more than 25 years. He’s sharing how he’s now helping people live well today in retirement without sacrificing tomorrow.

In this episode, Friends Talk Money co-hosts Pam Krueger, Richard Eisenberg and Terry Savage discuss what Medicare does and doesn't cover when it comes to treatments for Alzheimer's Disease and drugs for weight loss. A recent FDA decision means Medicare will be covering a new, game-changing Alzheimer's drug for many people 65 and older, but there are some strings attached. By contrast, Medicare currently won't pay for drugs to lower weight, although it will pay for weight-loss surgery in some cases. An act of Congress, however, could change the rules about Medicare and weight-loss drugs.

-

In this Friends Talk Money episode, college financing expert Mark Kantrowitz talks with our hosts Terry Savage, Pam Krueger and Richard Eisenberg on how grandparents can use 529 plans to save for their grandchildren’s’ college tuition bills.

-

A guide to who should consider buying a long-term care insurance policy, what these policies do and don't cover, what age to consider buying it and the newer versions known as hybrid policies and 10-Pay policies. Our guest: Brian Gordon, a long-term care insurance policy expert with Gordon Associates in Bannockburn, Ill.

For further research:

The Age Wave research and consulting firm and the Edward Jones financial services firm just published a survey of Americans’ views and actions regarding cannonballs and curveballs in retirement. In today’s episode we talk with Lena Haas of Edward Jones about the findings.

For further research:

-

Some retirees run into trouble receiving their promised pensions. Others aren't sure if they're eligible to receive pensions. Here's where to go to get help to ensure you get any pension you're due and to see whether there may be a pension waiting for you.

For further research:

Netflix released a new docuseries that reveals how Madoff got away with stealing $36 Billion from wealthy investors and charities.

It’s been 15 years since the biggest criminal on Wall Street, Bernie Madoff pulled off the largest Ponzi scheme in history. Bernie Madoff may be dead, but there are still plenty of con artists and investment scams and new lessons to learn from this story.

The clock is ticking towards Tax Day, April 18. Here are some timely tips for tax form procrastinators.

For further research:

Mention the word “annuity” and most investors recoil. There seem to be so many hidden secrets and costs. And high pressure sales tactics along with "free dinners."

In today’s podcast we unravel those mysteries – with the one man who has consistently worked to educate the public to the ins and outs of annuities – as well as some of the better uses of these insurance company contracts. Stan Haithcock’s website – www.StantheAnnuityMan.com -- is a great resource for free basic information and good advice on annuities. And Stan is one of the most entertaining financial speakers you’ll ever meet.

So, sit back and enjoy our podcast. We devote special attention to Multi-Year Guaranteed Annuities (MYGAs), now yielding over 5.5%. They’re the insurance industry’s version of a bank CD, without the FDIC backing. And they are a great way to improve yields either inside or outside your IRA.

To read more about MYGAs, here’s a link to Terry’s column on the subject: https://www.terrysavage.com/an-annuity-that-works-for-you-myga

And if you’d like to listen to more of Stan’s terrific approach to financial markets, both Terry and Pam have recently joined him on HIS podcast. You’ll find the links to these conversations here:

Terry Savage: The Savage Financial Truth in 2023

https://www.stantheannuityman.com/fwa-terry-savage-january-2023

Pam Krueger: Your Wealthramp to Fiduciary Advice

https://www.stantheannuityman.com/fwa-pam-krueger-february-2023

For further research:

Have you given some thought to where and how you’d like to live in your retirement years? Many insist on staying in the family home – without thinking about logistics of stairs and navigating the bathroom in later years. Maybe you’ll just downsize to a smaller home. Others decide to move into a senior community, making new friends in these settings with like-minded and active adults. The latest enticing option is Continuing Care Retirement Communities, which offer initial living in townhomes or condos, while guaranteeing acceptance for one or both spouses into assisted living or even memory care as the need might arise.

This is a financial, as well as logistical and emotional decision, as many of these CCRCs require a large up-front deposit, typically funded by the sale of the family home. Guarantees are involved, but you need to read the fine print. You’ll find an explanation and details in Terry’s recent column.

On this podcast, we will speak with Dana Smith, Chief Marketing Officer for Lifespace Communities (https://www.lifespacecommunities.com/), a non-profit company that has 18 communities in seven states, ranging from Florida to Texas, and Illinois to Kansas. As you’ll hear in this podcast, Dana has the answers to so many questions, ranging from how to get that deposit back to what happens if you run out of money. And she has tips on what to look for and what questions to ask if you are considering moving to a Continuing Care Retirement Community.

For further research: Next Avenue, Key Facts About Life-Plan Communities

Millions of Americans are feeling financially insecure about retirement, but "Retirement Reboot" author and journalist Mark Miller has some practical suggestions. In this "Friends Talk Money" episode, he shares insights and recommendations on: saving and investing for retirement, Social Security strategies, enrolling in Medicare and more.

Congress just passed a bill with the biggest changes for retirement in 15 years. The legislation, called Secure 2.0, has new ways to save for retirement and take money out of savings for emergencies, as well as new rules on how much you'll be required to take out of your retirement accounts and how the government will provide money to match retirement savings for some people. In this Friends Talk Money episode, we tell you what the new law means for you.

Many people worry about running out of money in retirement. But Jim Mahaney, a retirement advisor in New Jersey, says you can lessen that worry by creating what he calls a "resilient retirement income plan." He just wrote a whole book about it — "How to Craft a Resilient Retirement Income Plan" and in this episode, Friends Talk Money podcast co-hosts Richard Eisenberg, Pam Krueger and Terry Savage talk about how, and why, to do just that.

The holiday shopping season is officially underway, and like many grandparents and parents, you’re probablysearching for gifts that will make a lasting impression on young people–rather than being quicklyoutgrownor broken. So we have gathered some of our best holiday money gifts for kids of all ages—gifts that will keep on giving for years to come.

Delaying billing 2022 side-gig income until 2023, maximizing end-of-year pre-tax retirement plan contributions, and selling stocks at a loss to offset capital gains are just a few of many steps you can take right now to reduce your 2022 taxable income. Terry, Pam and Richard discuss these and other strategies and IRS changes that may lower tax bills for many Americans in 2023.

For further research:

With the stock and bond markets delivering lousy returns this year, some investors are wondering whether to add so-called alternative investments to their portfolios. In this episode, Pam, Terry and Richard discuss the risks of investing directly in unregulated asset classes like gold, real estate, commodities and even cryptocurrency and suggest ways that investors may be able to use publicly traded securities to gain indirect exposure to these alternative asset classes with lower risk.

Two thirds of retirees get more than half of their income from Social Security. That’s why it’s critical to make the right claiming decision. In this episode, the three friends are joined by Social Security expert and bestselling author Lawrence Kotlikoff, who discusses scenarios where you might want to start taking Social Security earlier or delay starting until your full retirement age or later.

For further research:

The housing market is a perilous place right now, especially for people over 50. Prices in certain areas are out of reach for many seniors who want to relocate, yet rising mortgage rates are making it difficult for many homeowners to sell at their asking prices. In this episode, Terry, Pam and Richard weigh the pros and cons of selling or staying put, various mortgage options, moving into a retirement community, and renting.

For further research:

What does the employment outlook look like for older Americans who will be looking for new jobs or want to hold on to the jobs they have? Will there still be remote or hybrid opportunities for those who don’t want to be in the office full time? And when today’s hot job market begins to cool, will there be a place for older employees in corporate America? To answer these and other questions, the three friends bring in two experts to discuss the future of the workplace and what those who want to participate in it may need to do to adapt.

For further research:

Many financial advisors are not doing much to help their clients prepare for retirement other than managing their investments. In this episode, the three friends discuss the many other ways a truly independent, fiduciary financial planner can holistically come up with a comprehensive plan to help retirees answer their many questions, from deciding when to start Social Security and choosing Medicare coverage to figuring out where and how they may want to live and determining an appropriate estate planning strategy.

In this episode, Pam, Terry and Richard discuss the pros and cons of socially responsible investing, whose increasing popularity is being driven mainly by women. In particular, they examine whether women sacrifice returns by investing in stocks or ESG funds that align with their personal values. The answer may surprise you.

For further research:

Janine Firpo, Activate Your Money: Invest to Grow Your Wealth and Build a Better World

Socially responsible investing made easy: https://newdayimpact.com/

Directly rolling over a 401(k) plan to an IRA with a custodian like Fidelity, Schwab or Vanguard is something most people should do as soon as possible after they retire. Why? Because most 401(k) plan investment options are designed for people saving for retirement, rather than for those who need their nest egg to generate income to help pay for everyday expenses. Rollover IRAs offer access to a wider variety of investment options, many of which may have lower expenses than the funds in your 401(k) account. But since you may need money in your IRA to last 20 years or more, you may not feel confident making your own investment decisions. A low-cost robo-advisor can automatically invest your rollover IRA money but won’t be able to answer your questions or address your concerns. That’s why it may be worth paying more for the services of a fee-only fiduciary financial advisor. They not only can manage your investments but can come up with a comprehensive plan to address the financial opportunities and challenges you may face during retirement.

For further research:

Since the 1990s an increasing number of people are getting remarried at a later age. Couples who are entering second marriages at this point in life need to fully understand the financial implications. How much wealth and debt will they bring to the union? Whose home will the newlywed couple live in? How do you make compromises on everyday spending and bill payments? And what should each person do to safeguard their own financial interests and those of their own children while still being fair to their new spouse and their children? Since money-related issues are one of the chief causes of marital friction and divorce, it’s important to have these discussions before the marriage takes place, even if the outcome involves establishing prenuptial agreements to protect both spouses.

For further research:

Recent research from the Employee Benefits Research Institute reveals that those most worried about financial security during retirement are Gen-Xers between the ages of 42 and 57 years old. With the market experiencing its worst start of the year since World War II, many are wondering whether the two-decade bull market is coming to an end. Others are worried that they’ll have to work longer than they planned. Or that the Social Security fund will be bankrupt when it’s time for them to start collecting. While there are actions Gen X-ers can take now to bolster their retirement nest egg, like maximizing contributions to 401(k) plans and IRAs and resisting the urge to reduce exposure to the stock market, many can achieve greater peace of mind by working with a fee-only financial advisor. These professionals can analyze Gen-Xers’ entire financial picture and recommend a plan to increase their chances of living the way they want to during retirement.

For further research:

If you want to work part-time in retirement, it's never been easier to find the kind of job you want. And it’s not just lower-paying, physically demanding jobs at retail stores and restaurants. With employers desperate to find workers, many are putting aside their biases against experienced and technically savvy older workers and allowing many to work at home or on their own schedules. And if you’re still working full-time but would like to ease your workload, your company may offer a phased retirement program that lets you gradually reduce your work hours over time while still retaining your benefits. Even if you officially leave your full-time employer, you may have the opportunity to work for them part part-time or as a consultant. However, the key to remaining a coveted part-time worker is to keep up with the skills that employers find valuable, whether it’s learning new technologies and staying current with the business trends in your industry.

For further research:

Ric Edelman, author of the new book “The Truth About Crypto” thinks everyone should have 1% of their investments in cryptocurrencies, including retirement investors. But the U.S. Department of Labor has concerns about allowing crypto in 401(k) retirement plans, just as Fidelity says it plans to let employers allow employees to put up to 20% of their 401(k)s in Bitcoin. The “Friends Talk Money” hosts talk to Edelman about all this and weigh in with their thoughts on putting retirement money into crypto.

Securities regulators estimate that at least 5 million elderly Americans become victims of financial fraud and other scams each year. With this kind of abuse only expected to increase, these regulators are strongly recommending that seniors formally appoint one or more children, relatives or friends as “trusted contacts” with their bank, brokerage company, financial advisor and other financial institutions. These trusted contacts can’t make transactions or even view their friends’ or parents’ accounts. They’re simply additional people the institution or advisor can reach out to if they’re unable to reach the account owners to inform them about suspicious activities or other account-related red flags.

For further research:

The S&P has been very volatile since January, after reaching many record highs over the past seven years. It’s hard for any investor not to feel overwhelmed and worried during these turbulent times. Watch nationally known financial commentators and co-hosts of the award-winning podcast Friends Talk Money, Terry Savage, Richard Eisenberg and Pam Krueger discuss how to stay focused during this market storm of inflation, the prospect for higher interest rates and global political and economic uncertainty in the aftermath of Russia’s invasion of the Ukraine.

Video link: https://vimeo.com/684698371

Mental health studies have shown that those who do nothing after retirement increase their chances of suffering from clinical depression by 40%. That’s why many retirees are choosing to “unretire.” This doesn’t necessarily mean going back to work full-time. Instead, it’s about filling your day with activities that bring you satisfaction. But to unretire successfully, you need to plan ahead, perhaps even before you retire. Here are five tips to get you started.

When it comes to COVID tests, vaccines and medical treatments, the way traditional Medicare Parts A and B pay for these expenses is not always clear cut. For example, right now Medicare only pays for four at-home COVID test kits that you order directly through covidtest.org. However, the Biden administration recently announced that in early spring Medicare will cover the costs of eight free test kits per month, the same number covered by private health insurers. Medicare covers the full costs of vaccines and boosters and the costs of having a healthcare professional administer the vaccine in your home. And if you get infected and need medical treatment in a hospital, Medicare Part A will cover hospital-related costs but you’ll still be responsible for any deductibles, co-pays or co-insurance. In some situations, Medicare might cover some home care costs related to COVID-19 but the rules are complicated. And traditional Medicare offers limited coverage for telehealth services. That’s why if you’re not sure of what is and isn’t covered contact the Medicare administration or your State Health Insurance Assistance Program.

For further research:

If you think that the stock market has been going through extreme positive and negative price swings over the past few weeks, you’re not imagining things. When volatility occurs, however, it’s important to resist the urge and flee to safety. Remember that, over the long term, stocks have delivered better long-term returns than bonds and cash. The question is: What percentage of your portfolio should be invested in stocks when you’re still saving for retirement or after you’ve retired? If you don’t feel that you have the knowledge or confidence to make these decisions on your own, consider seeking guidance from a fee-only fiduciary financial advisor. .

Fifty-four million Americans are over the age of 65. And extended life expectancies, coupled with low birth rates, are moving us toward a “super age” where more Americans will be over the age 65 than under age 18. With higher percentages of people likely to live well into their 90s, your retirement nest egg may need to last 30 years or more. Depending on how much you’ve saved and how you plan to live during retirement, you may need to make some adjustments, like leaving your full-time job at age 70 rather than 65 or working part time during retirement. In this super age, employers in particular will have to adjust to an environment where younger workers will be in short supply. Many will have to end ageist workplace policies and do what they can to retain experienced older workers or create attractive part-time opportunities for those who still have a lot to contribute professionally in their 70s and beyond.

For further research:

Go to any library or your local bookstore and you’ll see shelf after shelf of books offering practical education on various financial planning and investing. Sorting through these choices can be overwhelming, so Pam, Richard and Terry are here to help by sharing recommendations for money-themed books they have learned the most from. These books will help you fortify your personal knowledge of how to save manage and invest your money. While most of these books have been published within the past few years, several are classics that have been updated over the years.

Richard’s picks:

Terry’s picks:

From donating appreciated stock to establishing a donor-advised fund to contributing part or all of your Required Minimum Distribution from an IRA directly to a charity, there are many ways you can support the nonprofit organizations and causes you care about while also receiving significant tax benefits. However, before you give to any charity, it’s important to conduct background research to make sure the organization is legitimate and that they’re using most of their donations to fulfill their mission.

For further research:

Fidelity Charitable Gift Fund and Vanguard Charitable: Two relatively lower-cost donor-advised fund options

Whether it’s higher prices at the gas pump or at the supermarket, we’re all feeling the impact of inflation in different ways. Most economists predict that inflation will continue into next year, which could create extreme hardships for seniors living on a fixed income or for those who have had to use more of their retirement assets than they planned for. With the high likelihood of the Fed raising interest rates next year to tamp down inflation, these actions could put a damper on the surging stock market. That’s why now may be a good time to look over your portfolio to see if minor adjustments might be needed to reduce inflation risk in your investment accounts. For example, on the bond side you may want to invest in Treasury Inflation-Protected Securities (TIPS) or I-Bonds, whose interest rates rise or fall with inflation. Or you may want to add a small allocation to gold or gold ETFs, since this precious metal historically has served as a hedge against inflation and volatile stock prices. If you’re very speculative, you might even want to consider making a very small investment in cryptocurrencies. However, If you feel that your portfolio is allocated in a way that combines decent income generation from bonds and capital appreciation from stocks, and you have an adequate reserve of cash for emergency purposes, you may not need to make radical changes to protect against inflation, especially since no one really knows how long it will last. If you’re not sure what steps to take, a qualified fee-only fiduciary financial advisor can offer common-sense advice to help you better “inflation proof” your retirement nest egg without sacrificing its long-term growth potential.

For further research:

While those approaching retirement often calculate the total income they may receive from Social Security, pensions, 401(k) plans and taxable investments, many fail to consider the impact of federal and state taxes. For example, if you and your spouse file jointly and your combined income is more than $32,000, up to 85% of your Social Security benefits could be taxable. If you have a pension, you’ll have to pay taxes when it’s paid out to you. When you start taking mandatory or elective taxable distributions from your Traditional and Rollover IRA and 401(k) accounts, it’s important to know ahead of time whether these withdrawals will significantly increase your tax bill. If you take distributions from an annuity, any interest or earnings will be distributed first as taxable income before non-taxable principal. If you’re thinking of selling your home, you may have to pay capital gain taxes if the profit from your sale exceeds $500,000. And, of course, you may always have to pay taxes on income and capital gains you earn in your taxable accounts. Considering how all of these taxes could really add up, it’s important to start thinking about how to potentially reduce your future tax burden long before you leave the workforce. For example, if you plan to use your retirement money to pay off your mortgage sooner, instead of making one large one withdrawal, consider making a series of smaller annual withdrawals to keep you from moving into a higher tax bracket. Or, if you’re thinking about converting your Traditional or Rollover IRA to a tax-free Roth IRA, you may want to do this after you stop working but before you start taking Social Security benefits, when your annual income may be less. And you may want to change the way your money is invested in your retirement and taxable accounts to achieve an optimal balance of investment returns and tax management. Given the complexity of these decisions, working with an accountant and a qualified fee-only, fiduciary financial planner can help ensure that these challenges won’t significantly tax your patience—or your nest egg.

For further research:

From specialized piggy banks for younger children to establishing custodial brokerage accounts or Minor Roth IRAs for teenagers, there are a variety of ways you can give your kids a head start on understanding the importance of saving, investing and appreciating money this holiday season. And don’t forget the most important gift of all—a college education, which you can make more affordable by establishing a 529 College Savings Plan for each child. Earnings are never taxed and can be withdrawn tax free if they’re used to pay for qualified educational expenses. Each parent can contribute up to $15,000 per year per child with no gift tax implications and each grandparent can make one-time, gift-tax free contributions of up to $75,000.

For further research:

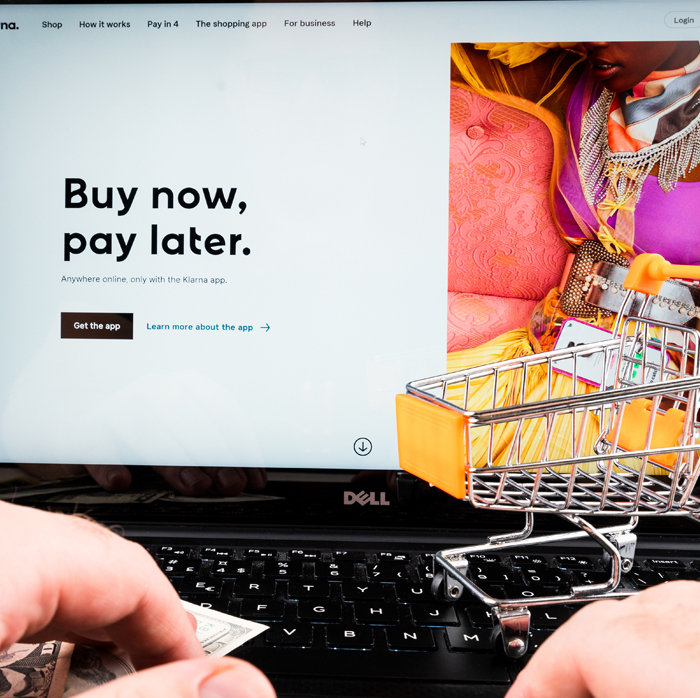

Since the start of the COVID-19 pandemic, 42% of consumers have increased the amount they owe for mortgages, student loans and car loans. The one bright spot is that the average amount of credit card debt has fallen during this time period. However, 54% of consumers with credit cards don’t pay in full each month and 18% owe more than $20,000. And the growing popularity of online “Buy Now, Pay Later" (BNPL) programs offered on many online retail websites such as Amazon and Walmart may end up increasing the mountain of debt many Americans are struggling to escape. According to research from Credit Karma, 40% of American consumers have used on these programs, and it's easy to see their attraction. BNPL allows consumers to make purchases now and receive the items right away, while paying them off in four payments. For people who are good at managing and paying off debts, these programs enable them to spread out the costs of purchases without taking on additional credit card debt. However, missing any of these payments can result in stiff late fees and interest charges. Credit Karma's research reveals that 34% of BNPL users have fallen behind on payments and 55% of younger consumers have missed one or two payments. Those who consistently miss payments for BNPL or credit card purchases may also be reported to credit agencies, which could seriously damage their credit score, making it even more difficult to be approved for future loans or credit cards. That’s why it’s critically important to safeguard your credit reputation. If you can, try to pay for online purchases with a debit card. If you use a credit hard, commit to paying off the balances in full each month. If you have outstanding credit card debt, try to reduce it as fast as possible, even if this means forgoing other purchases. And if you want to use BNPL this holiday season, make sure you make each payment on time.

For further research:

During the annual Medicare open enrollment period, from October 15 through December 7, you can make many changes in your Medicare coverage. But it’s important to understand the potential impact of making changes—or making no changes at all. First, if you’re in a Traditional Medicare program, you should sign up for a Medicare Part D prescription drug program within six months of enrolling in Medicare to avoid paying a late-enrollment penalty even if you’re not on any prescriptions right now. If you have Part D coverage already, it’s important to review your plan every year during this time to find out how much the annual premiums are rising or whether the prescription drugs you use now are still covered by the plan at the same costs. If your current plan no longer meets your needs and budget, consider switching to another plan that does. During the open enrollment period you can also switch from Traditional Medicare to an all-inclusive Medicare Advantage plan. While Medicare Advantage plans have lower premiums than Traditional Medicare, they’ll generally only cover physicians in their network and all requests for non-emergency care must be approved before they’ll cover the expenses. And if you have a catastrophic illness, you may end up having to pay up to $7,500 per year in out-of-pocket expenses billed by in-network healthcare providers—and up to $11,000 for out-of-network providers. That’s why it’s critically important to read the fine print and understand what is and isn’t covered by any Medicare Advantage plan and compare it to the costs of your current Traditional Medicare coverage. Fortunately, there are many resources you can turn for help in this complicated decision-making process. If it still seems overwhelming, considering working with a qualified fee-only fiduciary financial planner who can help you understand your various options.

Clarification: In the discussion of the maximum out of pocket costs for Medicare Advantage plans, listeners may have had the impression that Traditional Medicare plans don't have deductibles or co-pays. In fact, Medicare Parts A, B and D do have either deductibles, copays, or both. Unless you add supplemental Medicap coverage to cover these costs, you could end up paying significantly more out-of-pocket each year for critical medical care than with a Medicare Advantage plan, since Traditional Medicare has no annual cost caps.

For further research:

What makes people happy during retirement? Research shows that while financial security isn’t the most important thing, it’s near the top of most retirees’ lists. But it’s also important to think about what your life after full-time work will be like. Do you have social connections with whom you can share good stories and reach out to in times of need? Do you have enough outside interests, from hobbies to volunteering to keep you occupied? Do you have a plan B, such as thinking about part-time jobs that might interest you if you miss working? It’s important to think these things through because research also shows that unhappy retirees often feel that they no longer have a purpose in life or haven’t given enough thought about what they’re retiring into, rather than what they’re retiring from. In terms of financial security, happier retirees know how much they need to save to live relatively comfortably. They’ve paid off their mortgage or are close to doing so. And, they have several sources of income to rely on. A fee-only, fiduciary financial planner can help you figure out the financial aspects of retirement, but you may also want to seek out the services of other professionals who can help you anticipate the emotional aspects of retirement.

For further research:

The best time to start thinking about where you may want to live during retirement is long before you retire. While many people spend a lot of time pondering the kind of home they want to live in, they often don’t spend enough time researching the state, town or neighborhood where it may be located. But location may be the most important factor that determines how happy and healthy you’ll be in your new part-time or full-time residence. That’s why you’ll want to thoroughly research any locale you’re considering. How accessible stores and services are. The quality of local hospitals and healthcare professionals. Weather conditions. Whether your potential neighbors are the kinds of people you can make friends with and who can be counted on to help you in an emergency. How easy it is for your children and friends to travel there to visit you. Whether income, sales and estate taxes are lower than where you’re living now. How much of a mortgage you’ll need to take out if you plan to buy a new home. How quickly your home could be sold if and when you pass on or you need to move into an assisted living facility. Once your online research helps you narrow your choices down, plan on taking a trip to visit the top towns or neighborhoods on your wish list. If you find one you really like consider giving it a test drive by renting for a few months to get a real feel of what living there while could be like you’re still able to drive, shop, walk and go out at night. You might need to spend a year or more conducting all of this research, so it’s important to give yourself a head start before you actually plan to make your move.

For further research

Even though tax-deferred Traditional IRAs have been around since 1974 and tax-free Roth IRAs since 1997, you don’t hear a lot about them these days. Yet, for many people, especially those who are self-employed or don’t have retirement plans at work, IRAs still represent one of the best tax-advantaged ways to save for retirement. As long as you have earned income and your total annual income isn’t too high, you can contribute to an IRA every year. While both IRAs allow for tax-deferred growth, only the Roth IRA allows you to withdraw earnings and contributions totally tax-free at age 59½ or older. However, you make after-tax contributions to a Roth. While contributions to a Traditional IRA can be tax-deductible, you will have to pay taxes when you make qualified withdrawals after age 59½. And with a Traditional IRA, you have to start taking annual required minimum distributions (RMDs) at age 72, whereas you never have to take RMDs from a Roth IRA. But you don’t have to choose one or the other. As long as you have earned income and your Modified Adjusted Gross Income isn’t too high, you can open both a Traditional and Roth IRA. However, you can only make a total combined contribution of $6,000 each year ($7,000 if you’re over 50) to your IRAs. And if you already have a Traditional IRA or a Rollover IRA (funded with pre-tax assets you roll over from one or more company retirement plans) you’re not stuck with it. You can use a Roth conversion to move some or all of your Traditional or Rollover IRA assets into a Roth IRA. However, you will have to pay taxes on the converted amount, so it’s important to make sure the conversion doesn’t push you into a higher tax bracket. If you’re not in a hurry, you might want to wait to do it until the next market correction, when the value of your account will have fallen from its peak. And while there’s lots of talk about how tax proposals in Washington could potentially impact the tax benefits of IRAs, these changes will most likely only the wealthiest Americans. If you’re not sure which kind of IRA to invest in or how to complete a Roth IRA conversion in a tax-efficient manner, consider hiring a qualified fee-only financial planner. The fee you pay them for their guidance may pay for itself in the taxes you’ll save both today and down the road.

For further research:

There’s a common axiom that most financial decisions are based 1% on facts and 99% on emotions. Fear and stress of any kind, whether they’re job-related, pandemic-related, or financial security related, can impact our spending, saving and investment behaviors. Negative emotions lower our confidence, and the less confident we feel, the more likely we are to give into impulses, whether it’s spending more on alcohol, drugs or unhealthy food or panic-selling stocks when the market is falling. If you recognize the detrimental effects of negative emotions, you can begin to make plans to get your financial life in order. The best time to do this is when your life is relatively stable and the market isn’t going through gyrations. This may also be a good time to seek the services of a trustworthy, fee-only financial planner who can give you greater peace of mind by helping you confront the known and often unknown factors that cause fear and stress. They can offer objective, realistic guidance that lets you know where you are financially today and what you can do to improve your chances of achieving your short and long-term financial goals. But before you hire a financial planner, it’s important for you to set expectations for this relationship. What do you need the most help with: Cashflow analysis? Retirement, estate and tax planning? Investment management? Asset protection? The specific issues, stresses and fears you want to address will help you narrow your search to the kind of advisor who has the requisite skills, experience and resources.

For further research:

Social isolation, greater use of technology and the flood of stimulus checks and government aid programs during the COVID-19 pandemic have led to a dramatic increase of people victimized by cybercrime and financial fraud. Fraud reports received by the Federal Trade Commission in 2020 increased by 24% over 2019’s figures, from 1.7 million to 2.1 million. More and more Americans many of them elderly, are increasingly falling for online and phone schemes perpetrated by criminals posing as financial institutions, online retailers, government agencies and charities. These scams fool them into providing their Social Security number or other personal information or convince them to click on links that open the door for hackers to take control of their computers and mobile devices. The best way to protect yourself against these scams is to be ever vigilant. No legitimate company or government agency will ever ask you to provide confidential information in an unsolicited phone call, text, or email message. Get in the habit of immediately deleting any suspect messages or hanging up on any suspicious callers. If you’re uncertain whether the request is legitimate, look for the institution’s or agency’s legitimate phone number online and contact them just to be sure. Or seek advice from a friend or family member. And if you become a victim of financial fraud or identity theft, immediately contact your credit card company, bank and other financial institutions to freeze or close your accounts. Even if you avoid being scammed, you can still report these attempts to federal agencies or your local police department to help others from becoming future victims.

For further research:

Vanguard Funds’ John Bogle once said, “Investing should be boring.” During sustained market rallies, when the S&P 500 seems to hit new record highs every week, this often seems like good advice: Just set it and forget it. The problem comes when the market suddenly hits a period of turbulence. When this occurs, spooked investors often make bad mistakes—like selling stocks and stock funds at a loss. Anyone who bailed out of the stock market in spring of 2020 when the S&P 500 dropped by 30% only to see it fully recover by mid-summer learned a costly lesson about giving in to irrational impulses. So, how can you keep from making bad decisions? Well, just as the best time to get an umbrella is before it rains, the best time to start thinking about making changes to your investment portfolio is during periods of calm before a potential market storm. One good way to do this is to automatically rebalance your portfolio at least once or twice a year at designated times. For example, if the targeted asset allocation in your IRA or 401(k) account is 60% stocks and 40% bonds and rising stock prices have increased the stock allocation to 70%, consider selling 10% of your stocks or stock funds whose price you believe have peaked and use the profits to buy more bonds to restore that 60/40 mix. Or, if you’re close to retiring and realize you will need to withdraw more money from your retirement accounts each year than you originally expected, consider reducing your allocation to stocks when the market is still calm and move the proceeds into cash or money market funds. That way, if an extended bear market happens later on you won’t have to sell as much stock at a loss to generate the cash you need to live on. To make these decisions effectively you need to understand the connection between your investment strategy and your financial goals and have the self-discipline to make these adjustments even during volatile markets. If you don’t feel qualified to do this yourself, consider working with a fee-only fiduciary financial advisor. Entrusting them to keep your investment plan on track through all kinds of market conditions will give you greater peace of mind in knowing that your financial future is in good hands.

For further research:

According to Michael Clinton’s new book, Roar: into the second half of your life (Before it's too late), those who are approaching retirement should focus less on the idea of leaving the full-time workforce and more on what they can do to find the most fulfillment during this time. Whether it’s working part-time, starting a new business, taking up a new hobby, traveling, volunteering for causes your care about or mentoring young people, these various “layers” can shift your mindset from “retiring” to “rewiring.” And while you don’t need to be wealthy to enjoy a fulfilling life during retirement, meeting with a qualified financial planner can help you paint a realistic picture of what your finances will be like during your second half and which items on your “roar-wish- list” are truly attainable.

For further research:

Medical care is becoming a for-profit business even among nonprofit providers. Despite huge advances in technology, care is increasing impersonal, primary care physicians are getting harder to find, and patients are constantly being hit by “surprise charges” from medical procedures that are financially devastating. Many of these charges are unexplained up front and may be incurred by physicians, residents and fellows who are not part of your network. In this environment, it’s up to you to be your medical advocate, or ask someone you trust to serve in the role of healthcare proxy to come with you to appointments to ask key questions you may be too overwhelmed to ask yourself. When evaluating primary physicians or specialists, ask questions such as “Is your practice independent, or owned by a larger conglomerate?” “Does you or your practice receive compensation or special benefits from pharmaceutical companies?” “Are there ways for me to reduce costs, such as paying one co-pay that covers multiple visits?” “Can we meet virtually, and can I contact you via text or email?” Before you agree to any kind of potentially costly procedure, ask both your physician and your healthcare provider questions such as “How much will this procedure cost me out of pocket?” “Will all the physicians involved be in my network?” “Are there less expensive alternatives to an operation, such as physical therapy or prescriptions drugs?” And if it’s a major operation, you’ll want to be assured that the surgeon you’re consulting with will perform it, rather than a resident. If you or your healthcare proxy doesn’t feel they have the knowledge to sort through these issues, consider hiring an independent professional patient advocate or billing specialist.

For further research:

Some people describe the current economy by paraphrasing Dickens: It is the best of times, and it is the worst of times. On the plus side, the economy seems to be steaming forward, with robust job growth, increased consumer spending and a stock market that seems to set new records every week. Yet, in some regions and industry sectors, millions of Americans are still out of work and are facing foreclosures, eviction and the end of unemployment benefits. While inflation has picked up this year, it may either be temporary or long-lasting. While COVID-19 immunizations have allowed life to return to nearly normal in many areas, rising infection rates among the unvaccinated in many states are raising the specter of a return to lockdowns and business restrictions. While new infrastructure spending will help improve America’s crumbling roads, bridges and water supplies, the trillion-dollar cost will greatly increase the national debt to near record levels and may result in increased gas taxes and rises in capital gains taxes and taxes on the wealthy. Given these dichotomies, it’s hard to predict where the economy is headed, making it difficult for people to figure out what they should do financially to prepare for what may or may not happen. The best answer may be to simply take a good look at your personal finances and investments right now and see if there are minor adjustments you can make that will better prepare you for any outcome. For example, if you’re worried about inflation eroding the value of your nest egg, you might want to increase your exposure to stocks. If your stock portfolio is concentrated in larger companies, it might be time to sell some of the stocks (or funds that invest in them) and use the proceeds to gain greater exposure to midcap, smallcap and international stocks, real estate and even gold. If you’re worried about losing your job, start building up an emergency fund to pay for everyday expenses for at least six months or more, but don’t lock up that money in a CD where you’re barely able to earn any interest. If you’re paying down a mortgage, consider refinancing at today’s lower interest rates, before the Federal Reserve starts raising interest rates. If you’re unsure how to do this on your own, consider working with a qualified fee-only financial planner who can help you prepare for both the best and worst of times to come.

For further research:

It’s a common belief that owning a home is an investment, but the reality is otherwise. While the national year-over-year appreciation rate of 14.5% (as of April 2021) may seem high, this figure includes both areas where housing prices are skyrocketing as well as regions where appreciation is relatively low. Once you add the costs of owning a home—mortgages, taxes and home repairs—into the equation, the actual appreciation rate of the average home barely matches the inflation rate. So, for many people, their home not only isn’t an investment, but, depending on the never-sending cycle of home maintenance costs, it may end up being a money-losing proposition. That’s why you should think of your home solely as a place to live in, and one for which you need to set aside money each year for both ongoing maintenance as well as costly “surprises.” Making a list of when you last fixed your roof, had the exterior painted, installed a new furnace or central air conditioning system or bought a water heater, dishwasher or washer/dryer and estimating when they may need fixing or replacing can help you estimate how much you should put aside each year-- 1% of your home's market value may be a good place to start--and financially prepare you when these “surprises” occur. Having this rainy-day fund is important, especially during retirement, because the last thing you want to do is to tap into your retirement nest egg to pay for emergency expenses, especially if making a non-required withdrawal from your IRA or 401(k) plan assists could raise your taxes.

For further research:

Investment clubs are a great way for people to sound out investment ideas, ask questions, and increase their knowledge of the stock market with the help of friends and family members. The popularity of investment clubs, which started in the 1950s, has waxed and waned over the decades, but during the pandemic there has been a resurgence of interest. Social media and virtual collaboration tools make it easier for people to organize and participate in clubs. A new generation of no-fee trading apps enables people to buy fractional shares of expensive stocks with no account minimums. There are even dedicated sites that can help people form their own clubs or join other existing clubs. Some sites can even help clubs calculate investment results, maintain accurate accounting records and generate required tax forms. While participating in an investment club is fun and can help you become a more confident and knowledgeable investor, you should consider the money you invest to be “fun money” that you can afford to lose. The bulk of your investment assets should be invested in a diversified long-term portfolio that’s designed to align with your financial goals, rather than make quick profits.

For further research:

Thirty nine percent of those recently surveyed by Nationwide Insurance don’t know at what age they’re eligible to receive full Social Security benefits, and 70% said they wish they knew more about this complex topic. In general, if you don’t need Social Security income to make ends meet, there are huge advantages for delaying your benefits as long as possible. For every year past the minimum retirement age of 62 you wait, up to age 70, you’ll receive an 8% increase in payments. And if you wait until your full retirement age (65-67 depending on the year you were born) your benefits won’t get cut if you’re still working and earn over a certain amount. Unfortunately, these scenarios become more complicated at the household level. For example, if you and your spouse were born before 1954, you may be able to claim spousal benefits. If you’re divorced you may or may not be able to claim some of your ex-spouse’s benefits. And if your annual income is above a certain level, between 50%-85% of your benefits may be subject to federal taxes. It’s critical to view any Social Security scenario within the context of your overall life expectancy and retirement planning strategy, which should consider projected future expenses—including Medicare and long-term care costs--and additional income from part-time work, pensions, 401(k) plans and IRAs. Given the complexity of these issues, you may want to work with a fee-only financial advisor who can help you make more holistic retirement planning decisions. However, it’s important for the advisor to fully understand the rules around Social Security and Medicare. If they don’t, they should have access to accredited professionals who can help them—and you—make these critical decisions.

For further research:

The easing of the COVD-19 pandemic, increased consumer spending, supply shortages and continued government stimulus have resulted in the highest inflation rate since 1992. People are feeling its effects at the gas pump, at the supermarket, at car dealerships, at building supply companies and when they make hotel and airline reservations. But will inflation continue indefinitely, or even rise to the record levels of the early 1980s? Most economics believe it won’t. They predict that inflation will level off after consumers get their pent-up spending out of their systems, supply chain issues are resolved and pandemic-related stimulus spending eases. The Federal Reserve is keeping a close eye on inflation and is likely to increase interest rates and tighten the money supply if it sees inflation rising much beyond its target 2% annual rate.

While inflation does affect consumers’ pocketbooks, it’s important to remember that it’s a symptom of a recovering economy and that the inflation rates you see quoted in the news are year-over-year rates. This means that inflation today is being compared to the same period in 2020, when lockdowns and millions of lost jobs depressed consumer spending. Still, if you’re worried how inflation and rising interest rates could affect your financial security during retirement you may want to see how different rates could affect your current financial and investment plan. When interest rates rise, prices of existing bonds will fall, which means you may want to avoid buying long-term bonds or CDs. You may also want to increase your stock holdings, since, historically, stocks have outperformed inflation by a wide margin. If your mortgage rate is high, you may want to reconsider refinancing at today’s low rates even if this extend your payoff period by a decade or more. If you don’t feel comfortable making these important decisions on your own, consider working with a fee-only fiduciary investment adviser. They can stress-test your entire financial picture against various inflation scenarios and suggest actions you may want to take to reduce its potential impact.

For further research:

Next Avenue, Inflation and You: 8 Tips for Your Finances

Terrysavage.com, Where’s Inflation?

According to a new investor study from Ascent, 50 million Americans are likely to make their first investments in cryptocurrencies in the next year. The skyrocketing popularity of Bitcoin and other cryptocurrencies has convinced even former skeptics such as Warren Buffett that these digital currencies should be taken seriously. One reason why many doubters are becoming believers is because of the transformative blockchain technology that underlies cryptocurrency transactions. Blockchains are databases that record all transactions in a way that anyone can see and no one can delete or change, bypassing the need for banks, brokerage companies, or even advisors to serve as the middleperson for these transactions. Blockchains have become such a legitimate technology for digital transactions that even the U.S. government is now thinking issuing digital dollars at some point in time.

However, it’s important to remember that the reliability and transparency of Blockchain in no way lessen the highly speculative and unregulated nature of cryptocurrency trading. Those who are thinking about investing in any of the thousands of cryptocurrencies available may want to limit the amount of money they invest and treat it as a gambling activity—meaning they should be prepared to lose everything. Those starting out should stick with known cryptocurrencies like Bitcoin and Ethereum and use established exchanges like Coinbase and Kraken to trade them. Those who don’t feel comfortable purchasing cryptocurrencies directly may want to consider investing in exchange traded funds that invest in these digital currencies.

For further research:

93-year old Beverley Schottenstein trusted her grandsons to handle her $80 million investment account at JP Morgan but learned later, both the brokerage and her grandsons had made millions cheating her. Find out how in Part 2.

For further research:

NextAvenue, The Grandmother Who Won Her Elder Fraud Case Against Her Grandsons

Beverley Schottenstein is the matriarch of a billion dollar family empire. At age 93, she went into battle against one of the biggest banks in the world... and her own grandsons to teach them the lesson of their lives about much more than money.

For further research:

Twisted: Conflict, Madness, and the Redemptive Power of a Granddaughter’s Love

Only 17% of low and moderate-income adults aged 50 or older believe they are in good financial health, according to research from the Financial Health Network. Many of these people don’t have enough income or assets to work with a financial planner. This leaves them with many unanswered questions about how to manage their income and reduce their debts during retirement, how to choose Medicare coverage, and when they should start taking Social Security benefits. While robo-advisors can help people make smarter decisions about investing, these apps don’t address personalized financial planning advice. And while there still isn’t a single app that addresses all of these issues, there are many low-cost solutions that can address some of them, many of which also offer access to human assistance.

For further research:

According to the Employee Benefit Research Institute 2021 Retirement Confidence Survey, more than half of workers and a third of retirees said that debt was a major problem in their household. Too much debt can negatively impact your credit score, which banks and other lenders use to determine whether to approve your credit card or loan request and how much interest you’ll pay. That’s why it’s important to check on your creditworthiness on a regular basis. You’re entitled to receive one free credit report per year from each of the three main credit reporting agencies—Equifax, Experian and Transunion. Through April 2022, you can also receive free credit reports every week from these agencies. These reports will include your current FICO credit score, which is based on how much total debt you owe, your on-time payment record, and how long you’ve held different loans and credit cards. Any credit score above 700 is considered to be very good. Your credit score can change on a weekly basis, and the best way to raise it is by reducing your outstanding debt balances and making on-time payments. Another good reason to check your credit reports on a regular basis is to identify any errors that may negatively impact your score or to make sure that identity thieves haven’t opened fraudulent accounts under your name. To prevent future fraud, you can place a credit freeze through all three credit reporting agencies. This will prevent criminals from being able to open credit cards or loans using your stolen personal information, and you can “unfreeze” at any time. To help your children begin to establish their credit history without falling into a debt quagmire, encourage them to apply for a credit card with a low credit limit or one that’s secured by a deposit. And if you’re planning to co-sign a loan for a child or a relative, make sure you monitor their payments, since their delinquency will negatively impact your credit score.

For further research:

Most retirees want to live independently as long as possible. But it’s important to have realistic expectations of what you’ll be able to do on your own as you grow older. According to a University of Michigan survey of 8,000 seniors, 31% of respondents between the ages of 80-89 said they could live independently. That number dropped to just 4% for those over 90. If you’re hoping to live independently by staying in your home—or moving to a condo or townhouse in a retirement community—you’ll need to think about how you may eventually need to adapt your dwelling to accommodate physical limitations that naturally occur as you age. Fortunately, there are plenty of companies that specialize in installing stairlifts and making bedrooms and bathrooms wheelchair accessible. Mobile devices and smart-home technologies make it easier to get immediate help if an emergency occurs. If you’re living on your own, it’s also important to develop and maintain a multi-tiered social network of people who can help you—and whom you can help in return. Family, friends, neighbors and members of your house of worship can all play different roles in this network. Try also to build strong, mutually beneficial relationships with one or two younger people who are willing to help you during emergency situations. And make sure to formally designate people you trust to serve as your financial and healthcare proxies if and when you’re no longer able to make these critical decisions on your own.

For further research:

According to a recent MetLife survey, 19% of full-time Baby Boomers said they would need to delay retiring because of COVID-19-related financial challenges. However, in the same survey, 12% said that the pandemic had convinced them to retire earlier, citing reasons such as dissatisfaction with their job or “life is too short.”

There’s also a growing movement known as Financial Independence, Retire Early (FIRE). These workers, mostly highly paid Millennials and Generation Zers, are committed to saving and investing as much as possible and paring non-essential spending to the bone so they can retire in their mid-50s or earlier.

Whether you’re hoping to retire in your 50s or plan on working into your 70s, it’s important to evaluate whether you’ll have enough income to last potentially thirty years or more. Start by estimating your life expectancy, which is based on your family history as well as your current physical health and lifestyle habits. Next, consider whether you can delay taking Social Security until age 70, when you’ll earn the maximum benefits. Then calculate how much your 401(k) plan and IRA accounts will be worth at your desired retirement age and estimate how much of an income hit you might take if a bear market drives down the value of your retirement assets by 25% or more when you first start making withdrawals.

If there’s a strong possibility that you won’t have enough income from Social Security and your savings, consider whether it makes sense to invest some of your nest egg in an annuity that will provide guaranteed income for life or if you may need to delay retiring or take on a part-time job after you’ve stop working full-time.

These are complex issues and the cost of making the wrong choices today could threaten your future financial security. To give you greater peace of mind, consider seeking the advice of a fee-only fiduciary financial planner. These professionals can objectively analyze your current and future spending and income sources, your outstanding debts, and the size and holdings in your retirement accounts to provide a realistic assessment of how likely you are to achieve your retirement goals and what you can do to improve your chances.

For further research:

Many retirees allocate 60% or more of their portfolios to bonds, having followed the traditional mantra that fixed income securities are less risky investments than stocks. But what many are finding out is that with interest rates at historically low levels, the bonds they own may not be generating significant income and, in fact, may be hindering, rather than boosting, their portfolio’s total returns.

With money market instruments earning less than 0.5% and most long-term CDs earning less than 2%, the reputation of fixed-income investments as safe and reliable income generators has taken a beating in recent years.

Investors looking for a mix of credit quality and higher yields are having to seek out U.S. government and corporate bonds with maturities of ten years or more. But these long-term bonds carry risks as well. Should economic growth, rising inflation and reduced global demand for U.S. government bonds compel the Federal Reserve to raise interest rates in coming years, this will result in higher interest rates for new bonds and falling prices for existing bonds to make their relative yields more attractive. Long-term bondholders may end up losing money if circumstances require them to sell their bonds.

In this environment, investors may want to play it safer and look for CDs or bonds with maturities of six months to a year. While yields for these short-term securities will be lower compared to those of longer-term bonds, investors won’t have to wait as long (or potentially sell a bond at a loss) to reinvest their principal in higher-yielding bonds that may be available down the road.

If you don’t have the time or desire to buy individual bonds you may be better off investing in short to intermediate-term actively managed bond funds. Their portfolio managers are experts in buying and selling bonds to take advantage of different interest rate environments. But when comparing bond funds with similar characteristics and track records, you should closely scrutinize expenses and management fees. A fund with an annual return of 3% per year and 1.5% in annual fund expenses will deliver a net return for investors that is much lower than a similar fund or EFT that charges 0.75%. If you don’t feel comfortable doing this research on their own, you may wish to work with a fee-only fiduciary investment adviser. These professionals can objectively review your entire portfolio and recommend cost-efficient changes that will make all of your stock and bond investments work harder for your retirement.

For further research:

Clarification: When Terry mentions that during times of rising interest rates when an investor with a long-term bond "is stuck earning a slightly lower yield for the remaining 10 or 15 years or the life of the bond," she means that that this bond's yield will be lower relative to higher yields that may be available from newly issued bonds or existing bonds that are now priced lower. When an investor buys a bond, its yield is locked in and will never rise or fall for as long as they own it.

New research from EMD Serono’s Embracing Carers initiative found that 54% of family caregivers said that the COVID-19 pandemic has worsened their financial health. To help pay for their parent’s medical and living costs, children may have to use money they were saving for retirement or their own children’s higher education. If a caregiver has to quit a full-time job, this may reduce their future Social Security benefits and keep them from saving for their own retirement at work.

There are a number of ways parents and children can work together to ease this financial burden for both sides. First, parents need to help document all of their financial information, including location of assets, titles and deeds, attorney and accountant contact information, and life and burial insurance policies. Before a crisis occurs, parents should assign healthcare and financial power of attorney to their children to allow them to make key decisions when they’re no longer able to able to do so on their own.

Parents should also consider getting long-term care insurance to enable them to receive skilled care in their homes without consuming all of their savings. Some policies can be combined with life insurance to provide death benefits to heirs if the long-term care benefits aren’t used.

Children need to be sensitive in the way they bring up these issues. Start by offering to do small tasks, such as opening their parents’ mail or making sure bills have been paid. When it’s time to make major decisions, frame the discussion as a gift between generations: Children give their time to help their parents deal with declining health, and parents provide the financial support and cooperation to prevent this assistance from becoming a burden. To help sort through these complex issues, parents and children may wish to hire a qualified fee-only fiduciary investment adviser. But it’s important to research their background and licenses to make sure they’re not members of the large community of scammers and criminals who prey on the elderly.

For further research:

According to a recent UBS poll, 60% of women surveyed let their spouses and partners handle their finances. This is not uncommon, even among wealthy couples. The gradual shifting of financial responsibility and knowledge to one person often begins early in the relationship. But if the couple goes through divorce or the family financial manager dies or becomes physically or mentally incapacitated, their spouse or partner will have to scramble to figure out where their money is, how it’s being invested, and how debts are being paid while they’re also dealing with a legal or healthcare crisis. That’s why it’s important for couples to discuss these issues candidly and transparently, especially before retirement, so that either spouse or partner gains the knowledge they need to step in and manage their finances should a crisis occur. If this task is too challenging or contentious for a couple to do on their own, they should consider hiring a fee-only fiduciary financial planner to help organize and document their income, debts, savings and investments and serve as their impartial educator and mediator.

For further information:

Right now, millions of high school seniors are receiving acceptance letters and financial aid offers from colleges and universities. These offers usually include a combination of merit-based scholarships and grants, student loans, work study grants, and private parent loans. In past years, it was challenging to convince many schools to increase this aid. But according to author and college planning expert Ron Lieber, with the COVID-19 crisis reducing the number of applicants to most schools, parents are now in a better position to diplomatically ask for better offers. But this can be a confusing process. Parents need to negotiate scholarships and grants with the Admissions office, and loans and work study grants with the Financial Aid office. When meeting with these officials, parents should feel free to ask them to match or exceed the more generous financial aid offers their children have received from other schools. Even after students have accepted an offer, they should seek additional money by applying online for a share of the billions of dollars available through thousands of private grants and scholarships. Even with all this aid, parents’ share of their children’s annual college costs will still be significant. They should try to borrow as little as possible, particularly through private parent loans whose payback periods could last a decade or more. This is particularly important for parents who are approaching retirement age, since some of their Social Security benefits may be garnished if they’re unable to make monthly payments on their own. For parents with younger children, contributing to a 529 College Savings Plan as early as possible can give them a head start on building a reserve to help pay for future educational costs. Grandparents, too, can help by contributing to these plans or giving up to $15,000 a year per child without gift tax implications. The most important thing is to not let your fear about your children’s future or your guilt about what you’re able to afford keep you from making the right financial decisions.

For further research:

As Richard says, “It’s a doozy of a tax year.” The IRS will be way behind in issuing refunds, yet the deadline for filing your 2020 federal tax returns is still April 15. For most people, it will be filing as usual, but there are situations where special attention may be required. If you earned $75,000 or less ($150,000 as a couple) in 2020 and should have received a $1,200 government stimulus payment last year and a $600 payment in January but didn’t, you can claim these missing payments when you file your 2020 federal tax return. Even if you made no income last year, you still need to file if you want to claim these missing payments. If you donated to charity last year, you can deduct up to $300 in cash contributions even if you can’t normally itemize deductions. If you’re under age 59½ and took advantage of the CARES Act provision to take up to $100,000 out of your Traditional IRA or 401(k) account without early withdrawal penalties, you’ll still have to pay taxes on this withdrawal. But if you fully reinvest the amount you withdrew within the next three years, you’ll be able to request a refund for the taxes you paid. If you were one of the millions of Americans who received state unemployment benefits last year, you’ll have to pay taxes on those benefits. Unfortunately, if you were working for your employer at home last year, you won’t be able to deduct any money you paid for furniture, equipment or other job-related expenses. However, if your income declined significantly from previous years, you may qualify for tax relief. And if you’re expecting a refund or your missing stimulus payments, make sure you file electronically and allow the IRS to deposit this money into your bank account. Otherwise, you may have to wait months to receive the money you’re owed.

For more information:

In January, news from Wall Street was dominated by the GameStop saga. To put it simply, a group of individual investors belonging to a social media forum called WallStreetBets started buying shares of GameStop, a moribund online videogame retailer. This speculation drove the price up from $20 to nearly $500 in three weeks. The WallStreetBets clique pitched a Main Street versus Wall Street story, claiming that they were trying to punish hedge funds, which were making huge bets that the price of GameStop would go down. For a time this worked. Early investors became stock multimillionaires, and some hedge funds were on the verge of bankruptcy before the madness petered out and GameStop lost more half of its value by the first week of February. While the hedge funds ended up okay, individual investors who bought shares right before the bottom fell out were the biggest losers. This saga created a clamoring for regulators to step in and stop this kind of market manipulation, and focused industry ire on Robinhood, a popular, no-cost trading app that many of the WallStreetBets crowd used to buy GameStop shares. While this story is fun to read about, there’s no need for most retirement investors to lose sleep over it. The market is heavily regulated. Over the long term prices reflect what’s going on in the economy, and are rarely impacted by price gyrations among a few small companies. Investors who own a diversified portfolio of stock and bond mutual funds in their retirement accounts have even less to worry about, since these funds hold many different kinds of securities, so if the price of one goes down it will be offset by the rising price of another. If you do want to dabble in individual stocks, research each stock first to see if its current price reflects the company’s real value. If you buy shares, set a target price at which you’ll sell out and stick with it. That way, you won’t get stung when the bubble bursts.

For further information:

Note: The shownotes for this episode update and clarify some of the statements originally made in the podcast.

According to the Social Security Administration, the number of retirees who drew Social Security outside the U.S. jumped 40% from 2007 to 2017. While the COVID-19 pandemic has put the brakes on Americans’ plans to more aboard, once the crisis is over there’s likely to be an explosion of retirees choosing to live outside the U.S. part of the year or permanently.

While it’s fun to dream about spending your retirement years in Europe or in a tropical paradise, there are many issues you need to think about before making such a life-changing decision. Your Medicare plan may or may not provide coverage in foreign countries, so it might be necessary to purchase supplementary medical insurance. Even if the nation you’re considering offers free or low-cost government-subsidized healthcare, you may not be eligible for it as a non-citizen. And the quality of physicians and facilities in that country may be inferior to those in the U.S.